One Big Beautiful Bill Act

By: Aaron Anderson, CFP®, CFA, Managing Partner

September 29, 2025

Normally I focus my end of quarter article on what happened last quarter and expectations for the next one. The interesting thing about writing so often and history tending to repeat itself is that I realized I’ve already said everything I was planning on saying.

September is traditionally the weakest month of the year. If there was a reason to time the markets, that might be one. Last quarter the market was optimistic over Fed rate cuts and so September was a strong month showing another reason why we don’t try to time the markets.

For next quarter, more rate cuts are expected, but a big concern is a looming government shutdown if Congress can’t agree on a funding bill over the next few days. However, we’ve seen this one before too. While there may be some volatility during the shutdown, the market tends to shrug them off especially looking a year out from the end of the shutdown.

So, instead, I’ll focus on the other big news from this quarter – the One Big Beautiful Bill Act (OBBBA). The bill is around 900 pages long, so before touching on some of the important highlights, I want to mention that like with any new law, regulators must still interpret the law to put it into practice. So, some of what is stated here might change as that process plays out. I also wanted to warn you that due to changes in the bill as it passed through Congress, there are a lot of articles with information that did not make it into the final bill. Be careful what you read or send it to me for review if you want.

Things made permanent: Some things from previous bills that were set to expire at the end of this year were made permanent: higher standard deduction of $15750 for single filers and $31500 for married filing jointly, deductibility of mortgage interest capped at $750k of indebtedness, current tax rates and inflation-adjusted brackets, estate tax exemption at $15M for individuals and $30M for couples. Some of that will be inflation adjusted each year. As with anything, these are only permanent until a future bill makes them not permanent.

Senior Deduction: One of the original selling points was no tax on Social Security but instead it ended up as a deduction for seniors of $6000 individual and $12000 married filing jointly. The important thing to point out is that these are deductions not credits. So, if you are in the 22% bracket, a deduction of $6000 would result in only $1320 less in taxes. There are income limits above which the benefits are reduced and this goes away in 2029.

SALT Limit: One of the points of contention in the 2017 Tax Cuts and Jobs Act for those who itemize deductions in high tax states was the $10k cap on deductibility of state and local taxes. This has been raised to $40k and increases by 1% per year through 2029 after which it reverts to $10k. As with the senior deduction, there is also an income limit phaseout.

Charitable Contributions: Two changes of note here. The first one that affects everyone who donates to charity is that non-itemizers can now deduct $1000 single, $2000 married filing jointly in cash charitable contributions. So, if you don’t usually itemize and so don’t keep receipts from your church or other charitable organizations, you should start doing so. The second is that for people who do itemize charitable donations, the first 0.5% of your adjusted gross income would not count. As a simple example, if your AGI is $100k and you made $5000 in charitable donations, then the first $500 in charitable donations would not count and only $4500 would.

Children & Education: The child tax credit has been increased to $2200 per child and includes inflation adjustments. Prior to the OBBBA, up to $10k of tuition would count as a legitimate expense for 529 accounts for a K-12 student. This has been expanded to $20k starting in 2026 and includes other things like books, online education materials, and tutoring.

Trump Accounts: Starting no sooner than July 2026, people can open a Trump account for a child under age 18 and can contribute up to $5k per year into it. For children born between 2025 and 2028, the federal government will also make a one-time $1000 deposit into it. Generally, there are to be no withdrawals before age 18 and when the child turns 18, the rules around traditional IRAs apply. The House version of the OBBBA originally earmarked these accounts for use in starting adult life – college, vocational training, starting a business, buying a house, etc – but the final version makes it more like a retirement account.

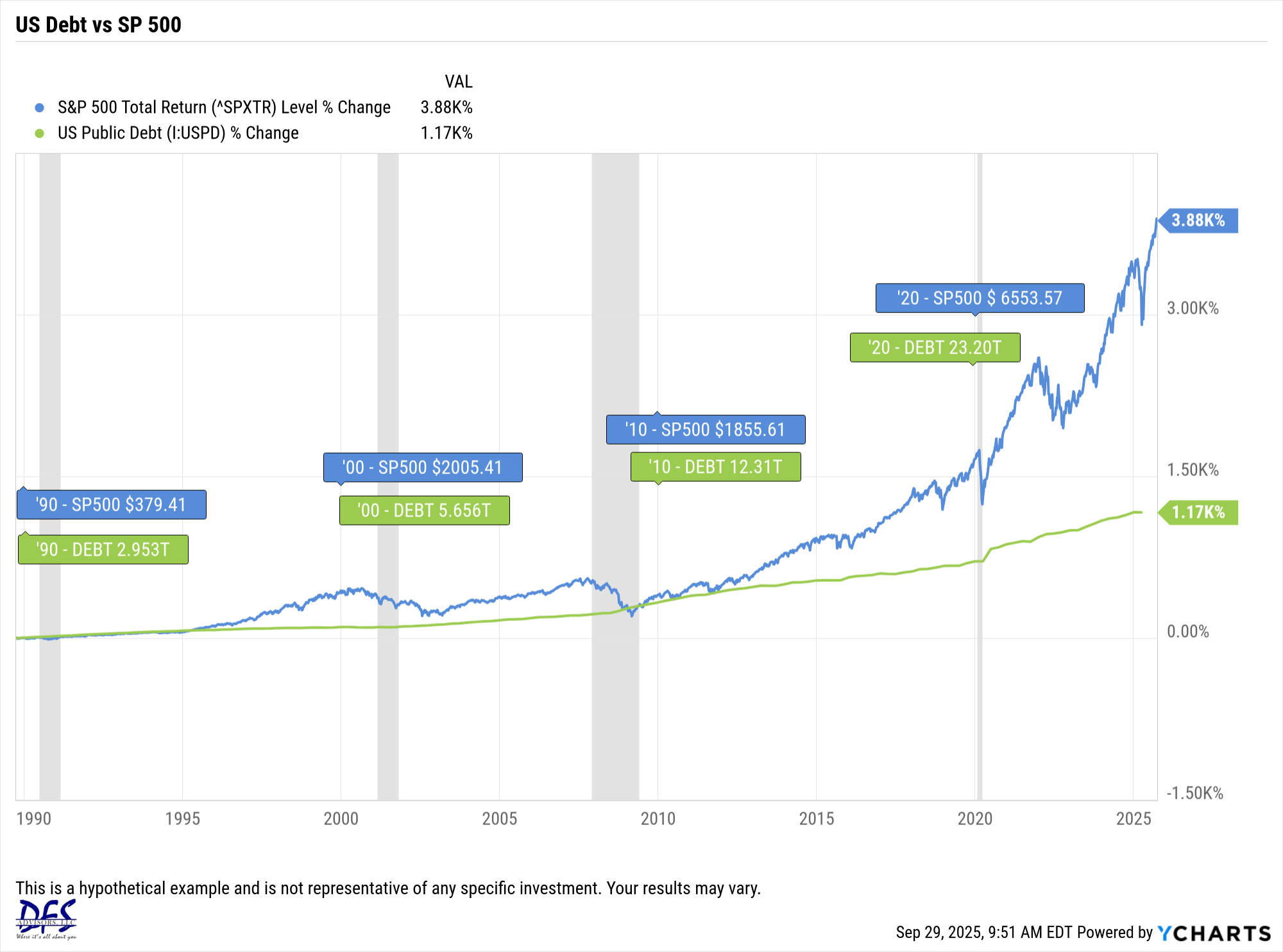

While this article mainly focused on taxes, I want to end by tying it back into investing. The Congressional Budget Office estimates the OBBBA will add $3T extra to the national debt over the next decade. The debt is already at $36.2T. To give you an idea of how truly staggering that number is, please see the end of this article I wrote two years ago where it gives a visual of what the national debt looked like at the time. Should we be concerned with the debt and its effect on the markets?

Historically, the answer is no. When I was a kid in the 1980s and 90s, I remember how people were upset with the national debt then when it was "only" $3T total. But as you can see on the following chart that compares the total return of the S&P 500 to the national debt, the market did well despite the rising debt. I do think it could eventually be something that causes the market trouble, especially if we get serious about a balanced budget or paying off the debt. However, had someone used the growing national debt as a reason to not invest in the market all those decades ago, they would have missed out on what has arguably been one of the best bull markets ever - and this includes the "Dot Com Bust" in 2000 and the "Great Financial Crisis" of 2008.

Since tax policy changes have historically had little impact on long-term investments and fear around debt has been an investment headwind for decades, we believe investing in a well-diversified portfolio aiming to weather various economic conditions still remains a good approach for building long-term wealth. As always, please feel free to reach out with any questions or to discuss.

Content in this material is for informational purposes only and not intended to provide specific advice for recommendations for any individual. All performance referenced is historical and is no guarantee future results. All indices are unmanaged and may not be invested into directly.

The Standard & Poor's 500 Index is a capitalization weighed index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing includes risks, including fluctuating prices and loss of principal.