2025 Outlook

By: Aaron Anderson, CFP®, CFA, Managing Partner

December 31, 2024

2024 was another good year for the markets with its second consecutive year of 20%+ returns, but it was a bit of an odd year. Election years tend to have a lot of volatility going into the election until the market gets more certainty, but not this year as it mostly marched higher with short, small drawdowns. The maximum intra-year drawdown was only 8.5% and that occurred in July which is a typically strong month. The September weakness that has occurred with regularity over the last few years did not materialize. The market is down 2.3% this month despite an 83% historical probability of gains during presidential election years in December.

So what does that mean for 2025? It would be a mistake to assume that two above average years in a row warrants a bad third year. One only has to look back to 2019-2021 where we had three years in a row of above average returns. There were five years of 20%+ returns in the late 1990s. While that run didn’t end well, it would have been a mistake to sell out after the second year despite the subsequent losses of the dot com bust.

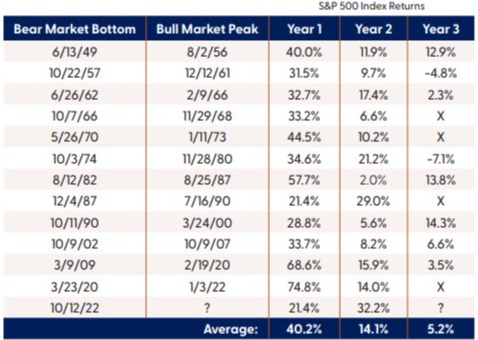

One of the many benefits of our partnership with LPL Financial is access to the LPL Research team. In their recent “Outlook 2025” piece, they present the case of a positive but modest year. Assuming we don’t have a recession, year three tends to be good for bull markets although the average return was a modest 5.2%.

Interest Rates: As we’ve discussed previously, the Federal Reserve started cutting rates in September. They cut rates again in December, but decreased their expectation of the number of rate cuts for 2025 from four to two due to possible lingering inflation pressures. The market responded as expected which helps explain why it was down in December. However, during the 12 months following the first cut in a Fed cycle, the S&P 500 has produced 5.5% on average – double that without a recession.

Stretched Valuations: While earnings have grown over the last few years, the price of stocks has increased at a faster pace. As a result, the P/E (price to earnings) ratio for the market has gone from around 20 at the bear market bottom in October 2022 to around 30 today. That does not necessarily mean that stocks are overvalued and will drop as the P/E ratio can continue increasing if market sentiment remains strong. With expected earnings per share growth for the S&P 500 in the 10-15% range, it can mean muted expectations as earnings grow into those valuations.

Trump 2.0: There have already been discussions about reducing regulations and cutting taxes. One concern over the past few years has been the 2025 sunsetting of the tax reductions from the 2017 Tax Cuts and Jobs Act. Extending those tax cuts are likely to be a priority of the new Congress and administration which could be good for stocks. But Congressional Republicans also showed some fiscal discipline in the recent budget negotiations. If they do look to lower fiscal spending from the high levels we’ve had recently, that could also temper economic growth and thus stock price growth.

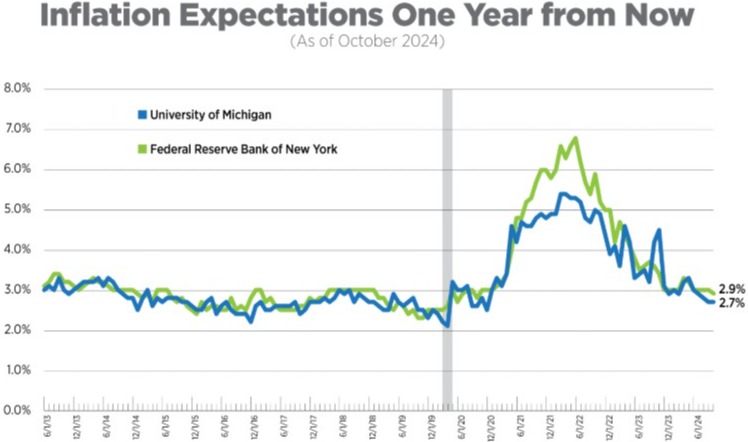

As optimistic as I am about the market long-term, I would be remiss if I ignored some of the negative things that could cause next year to be a bad one for the markets. The biggest is reaccelerating inflation. If that happens, then the Federal Reserve would likely raise rates again to avoid what happened in the 1970s. Fortunately, inflation expectations one year from now are around 2.7-2.9% which, while higher than the Fed’s target rate of 2%, is less than current inflation numbers.

There’s also the risk of Trump’s tariff threats turning into real tariffs, people selling instead of staying invested while earnings grow into valuations, or Congress being unable to pass business friendly legislation or even continue funding the government when it comes up in March. And of course, there’s always the ever-present concern that the current wars around the world expand into something more engulfing and harmful to the world economy than they are now.

While we can’t consistently predict the future, we can invest and set our expectations based on probability and history. I’m hoping for another great year for the market like we’ve had in the last two. Three in a row has happened before and could happen again, but looking at history, it is more probable that we’d have a modest year of returns.

Whatever the market does, I hope you and yours have a happy and healthy year!

Content in this material is for informational purposes only and not intended to provide specific advice for recommendations for any individual. All performance referenced is historical and is no guarantee future results. All indices are unmanaged and may not be invested into directly.

The Standard & Poor's 500 Index is a capitalization weighed index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing includes risks, including fluctuating prices and loss of principal.