More of the Same?

By: Aaron Anderson, CFP®, CFA, Managing Partner

January 3, 2024

Wow, what a good last quarter! We had nine straight weeks of gains for the market – the longest stretch of positive returns since 2004. Once the market got some clarity from the Federal Reserve that inflation seems to be moderating and more rate hikes are likely not necessary, it was off to the races.

The Fed seems to have been able to pull off – at least for now – what many thought was impossible. They were able to get inflation under control through one of the fastest interest rate hike cycles in US history without derailing the economy. The recession that everyone predicted for 2023 never materialized. Almost everything seemed to go well, a fairy tale ending.

In my last article, I hoped that the last quarter would be a good one for markets based on history and I'm glad it happened. Forecasts can be as accurate as the random answers from a Magic 8 Ball, but from my perspective, these are some possible outcomes over the next year looking at market and economic history.

I’m sure this will come back to haunt me, but here goes:

- The first quarter may likely be volatile. We just came off of a stupendous quarter. It stands to reason that people will take profits and then weaker hands will sell at the first sign of market weakness. It’s rare for the markets to do as well as they did for so long without some sort of reversion to the mean. We also have the same political risk that’s been lurking in the background for the last year – Congress and a budget, or lack thereof. As before, I expect there to be brinkmanship around it but since it’s an election year, I do think they won’t purposely kill their election chances by shutting things down. Speaking of election years…

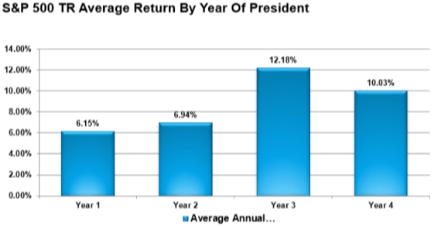

- The market should have a good return this year despite the election. No politician says how great America is during an election year. The nonincumbents trash the US to try to say how they will fix everything. The incumbents, while trumpeting their achievements, will also point out all the negatives to show there is more to do when they get reelected. It’s hard to hear all that negativity and not start internalizing it. But, as this chart shows, election years tend to be good for the market (source). Of the four years in each presidential election cycle, they average second best.

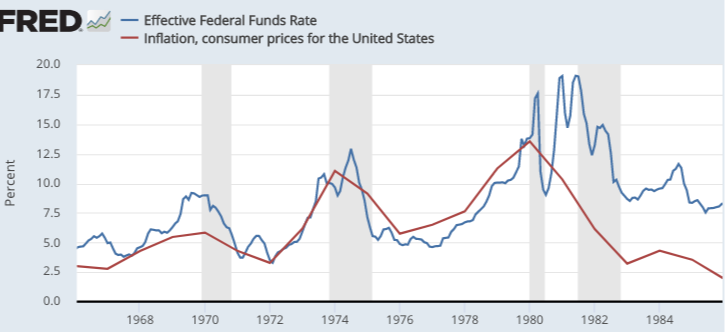

- The Fed might lower interest rates but I don’t think they will meaningfully. They expect to lower rates by small amounts three times in 2024. That’s one of the reasons the market has done so well over the last two months. But lowering rates is a way to juice the economy which it doesn’t currently need. Plus, they also don’t want to repeat the mistake of the 1970s. As you can see from the below chart, inflation started to be an issue early that decade. They thought they raised rates enough to control it and took their foot off the brake too early. Inflation soared in the later part of the decade and it took raising interest rates to extremely high levels through the early 1980s and pushing the country into recession to tame it. While I would love 20% interest rates in my bank account, I definitely don’t want the out-of-control inflation that caused the Fed to raise rates to those levels or the deep recession that usually follows!

- Continue investing for the long term. I know, I know, we always say that, but history has shown it to be an easy prediction to make. So, despite all of the doom and gloom you see on TV to juice ratings and ad revenue or what you hear from politicians looking to get elected this year, your portfolio should be able to weather it if you have the discipline to stick to your plan.

Content in this material is for informational purposes only and not intended to provide specific advice for recommendations for any individual. All performance referenced is historical and is no guarantee future results. All indices are unmanaged and may not be invested into directly.

The Standard & Poor's 500 Index is a capitalization weighed index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing includes risks, including fluctuating prices and loss of principal.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.